Market update: October 2022

.jpeg)

October proved volatile but was much rosier than September. This was due to a positive sentiment in the market - among investors - that the series of interest rate hikes might be coming to an end. Despite the fact that inflation showed no signs of slowing down and the disappointing quarterly results of large tech companies such as Meta Platforms and Amazon.

Politics also played an important role this month. Whether it was through the election of Xi Jinping to a third term. Or through the appointment of Rishi Sunak as the third prime minister of the United Kingdom in just two months. And although politics exerted considerable pressure, the European Central Bank (ECB) doubled interest rates by 0.75%.

Stocks in emerging markets performed less well because investors are concerned about China's growth forecasts. Worldwide, investors fear a short-term focus on power instead of growth by the newly appointed 'standing committee' in the government of China.

Bond yields initially rose in the US and Germany but cooled off in the second half of the month due to changing sentiment.

Best fund performances in October 2022:

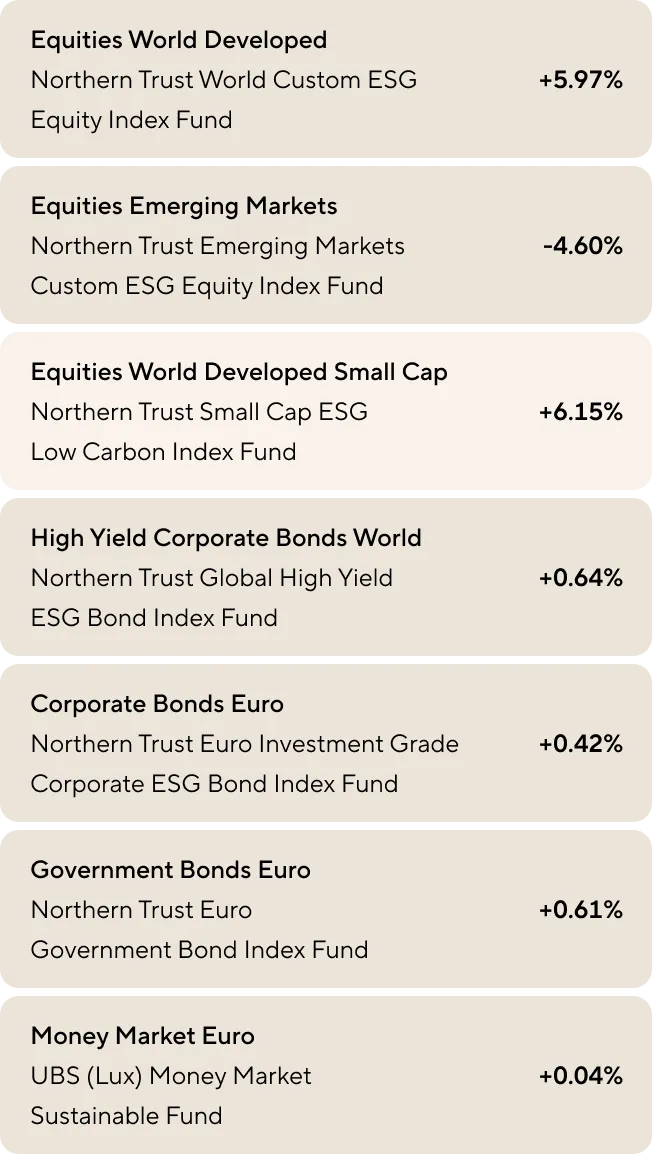

NT World Small Cap ESG Low Carbon Index Fund +6.15%

Banks and energy companies outperform tech giants, central banks continue to raise interest rates in their fight against inflation.

Stocks in developed countries bounced back from the disappointing month of September. After nine consecutive weeks of outflows from global equity funds, there was - in the last week of October - a renewed surge in investment.

According to Refinitiv Lipper (a reputable financial service provider that offers impartial performance data on, for example, pension or equity funds), the net inflow in that week totalled approximately $7.8 billion.

The S&P 500 closed the month 9.2% higher. Inflation in the United States was still higher than expected in October (8.2%). However, the market was supported by growing optimism that central banks will raise interest rates at a slower pace. That's because:

- The Bank of Canada implemented a smaller interest rate increase than expected (0.5%).

- Christine Lagarde (ECB) expects the Eurozone to enter a recession.

- FED governors shared that interest rates will rise less quickly again.

Stocks in Europe followed their American counterparts (STOXX 600 +6.3%).

Liz Truss resigned as Prime Minister of the UK. Rishi Sunak was appointed as her successor with the challenge of getting the British economy back on track. The British pound recovered slightly (1.15 GBP vs. 1 USD) after the election. And there was some short-term breathing space for the British government to borrow money to recover from Brexit and Covid as interest rates on bonds fell.

Emerging Market equities performed worse than the 'developed' ones. China remains a concern for investors worldwide. It is expected that the newly appointed 'Standing Committee' will focus more on power than growth in the short term. In addition, the persistent Covid-19 restrictions for China appear to be a challenge to returning to their economic growth.

India and Korea, on the other hand, did better, but TSMC (the chip manufacturer from Taiwan) struggled throughout the month due to a predicted decline in chip demand and lower expected investments in the coming quarters.

The price of crude oil rose (+11%) because OPEC+ has limited the pumping of crude oil to 2 million barrels per day. Other commodities such as gold and silver are not changing as much, despite developments in sentiment.

US and European 10-year yields rose sharply, with 24 basis points in the US and 4 basis points in Germany. Thanks to the perseverance of global central banks to combat inflation by implementing interest rate hikes.

High-yield bonds (+0.64%) and corporate bonds (+0.42%) showed a relatively slightly better result, with a decrease in the risk premium during the month due to the positively influenced sentiment.

Money market rates rose after the interest rate doubled. The money market return is expected to continue rising to a level of 1.5% next month after the next interest rate hike.

What does November have in store for us?

- Meeting of the Federal Reserve (FED)

- Ongoing developments in the situation in Ukraine

- Economic data indicating less inflation and a lower chance of recession as a starting point for continued optimism.

What does all this mean for my plans?

Don't let the market disrupt your long-term goals. Vive's investment strategies take the declining market into account. Ultimately, well-diversified portfolios are the key to long-term success. Consistent periodic investing in periods like these is crucial to take advantage of falling markets.

maak een afspraak

Klaar voor een moderne oplossing voor pensioen of vermogen? Maak vrijblijvend kennis met Vive en ontdek wat kan - voor jouw organisatie.

Complex pensioen, simpel uitgelegd - weet direct waar je staat

Persoonlijk gesprek voor jouw situatie en die van je werkenemers

In 30 minuten meer duidelijkheid dan uren googlen

Alle ruimte voor vragen aan onze ervaren pensioenexperts