War, inflation and the World Cup. What to do with your money in uncertain times?

.jpeg)

What to do with your money in uncertain times?

One of the biggest challenges of investing is dealing with uncertainty and market fluctuations. China’s strict covid-19 policy and the pressing situation in Ukraine are the leaders of uncertainty this year. With inflation, rising interest rates and increased food and fuel prices as a result.

You can see these effects in society and on the global stock market. The MSCI All Country World Index (MSCI ACWI Index) is an indicator for the global market, with shares in both developed and emerging markets. Since the beginning of this year (YTD), the index has fallen by ~16%. Reason enough for investors to wonder what to do with available and invested capital. What do you do with money in your (investment) account now?

Rest assured. The economic uncertainty that grips the world now is, in a sense, not new. In the past, there have been several financial crises.

Such a downward movement of the market is part of what investors call a 'market cycle'. A period that usually lasts five to seven years and consists of an upward and downward movement of the market. Although it is not clear in advance how long the cycle will last exactly. The past shows that there is light at the end of the tunnel. So perseverance is important in uncertain times. But how does it work?

Contributing periodically pays off

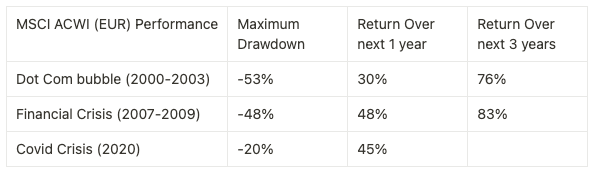

Consider the last three major crises through the lens of the aforementioned MSCI ACWI Index. The Dot.com bubble, the Financial Crisis, and the Corona crisis have something in common. The performance over a period of 1 to 3 years is remarkable.

People who were able to continue investing during such a difficult period - in which the markets collapsed - saw a significant increase in the value of their investments in a relatively short period of time. Research shows that contributing periodically to your investments (for 6 to 12 months) during a crisis works better than investing once when things are going well. The best way to do this is with a solid plan.

It always starts with a plan

“What’s needed is a sound intellectual framework for making decisions and the ability to keep emotions from corroding that framework.” - Warren Buffet

What the world-famous investor and CEO of Berkshire Hathaway means is simple. Successful investing starts with the right plan of approach. Such a plan consists of two parts.

🧭 A strategy that determines how you achieve your long-term goals and what your approach is in different situations. This helps you stay disciplined in times like these, so that emotions don't get in the way of your goals and you don't get out (too quickly) or lock in your losses.

🧇 A portfolio that matches your goals and strategy. This is a distribution of different types of investments, such as stocks, bonds and cash. You can adjust the composition as needed (rebalancing). By rebalancing, you adjust the portfolio to the market conditions to take (temporarily) more or less risk and thus protect your assets or increase the chance of return.

In short, to invest in uncertain times – so that you achieve your long-term goals – you need a plan. With a strategy and a good portfolio composition. So that you are less sensitive to the market and your emotions. Because despite the fact that it doesn't feel like it now, there is light at the end of the tunnel in this crisis as well.

Diversification protects assets

You put together the portfolio of your plan through diversification. This is a tactic to manage (investment) risk, because you create a mix of different investments in a portfolio. Instead of concentrating your assets in one company, share, sector or industry, it is wise to spread your investments as much as possible. Across different companies, industries and 'asset classes'. An asset class is nothing more than a type of investment such as shares or bonds. But it can also be real estate or crypto.

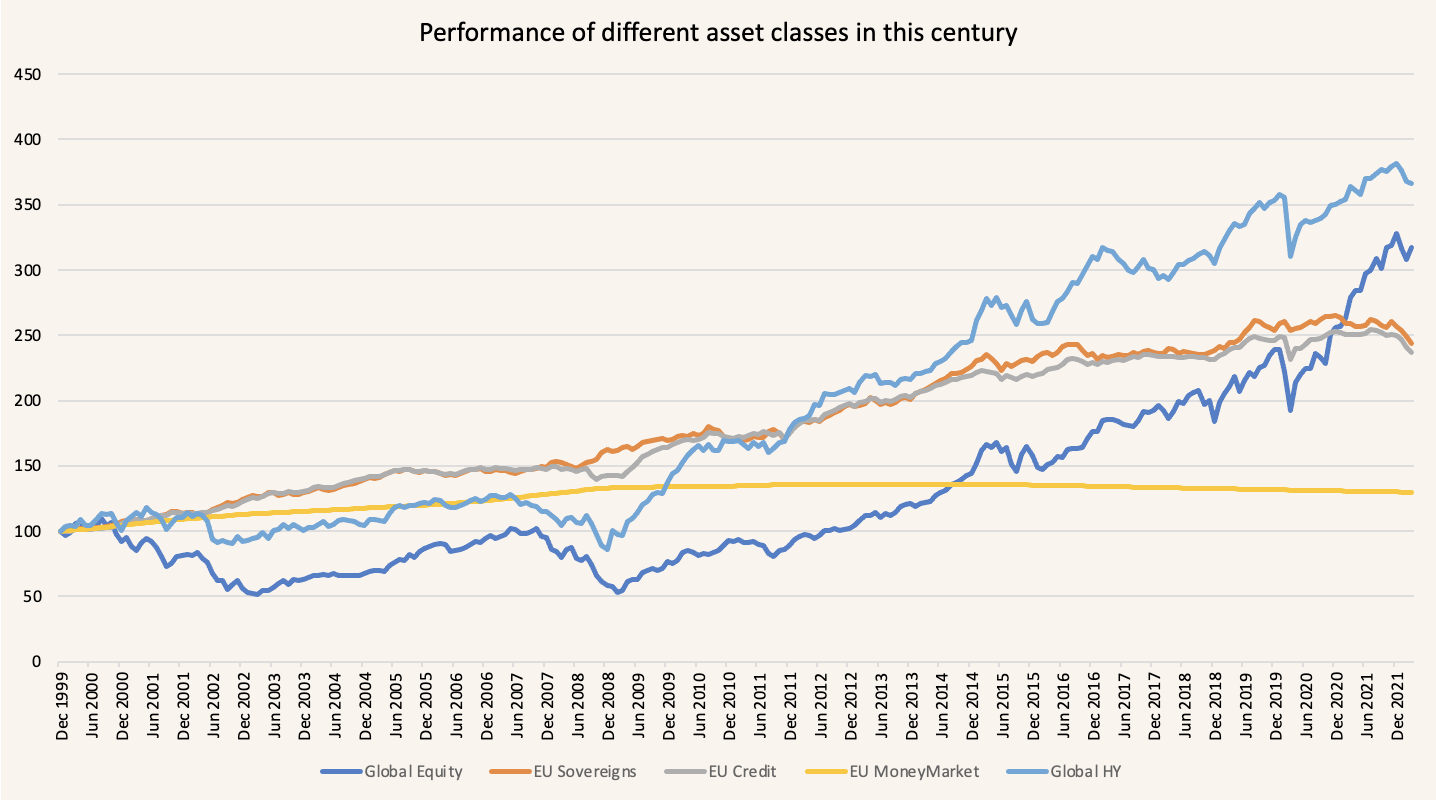

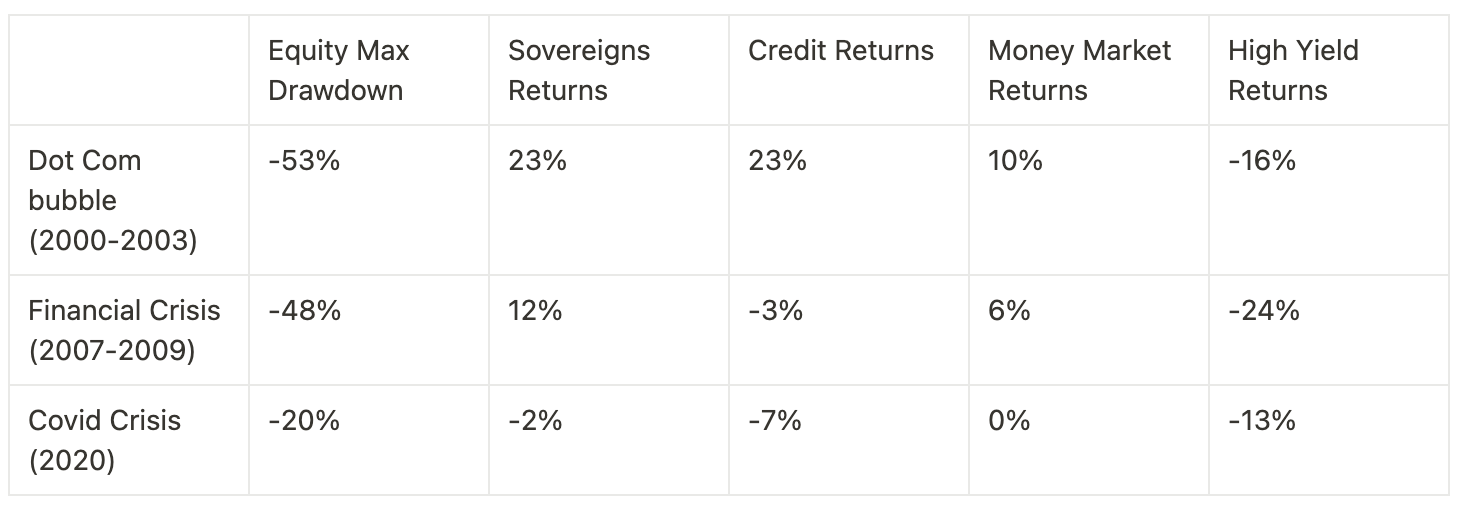

Spreading your investments works to your advantage, because investments will not all develop in the same way over time. Take a look at this figure.

You can see that during the less favorable periods, in which the return on equities was quite poor, the results of other asset classes were significantly better. Looking at the table below, you can see that this principle even applies during the three major (financial) crises. If your portfolio at that time consisted of a good mix of equity and bond funds, you would have lost less money, simply put, than if you had only invested in 'equity'.

As an additional advantage, by diversifying, you also had more capital to deploy as soon as the (stock) markets improved again. Despite the fact that it is obvious not to bet on one horse - this remains an insight that many people overlook.

Do you already have a well-diversified portfolio in a time of high market volatility? Then it may be wise to rebalance your portfolio so that the risk of your portfolio matches your goals.

Why not leave money in the bank?

It's obvious that inflation is rapidly making everything more expensive. As you can see in the table below, and already know, the savings interest rate in the Netherlands has not really started to move yet.

That means tough times for the money in your bank account if you don't do anything with it. In the financial market, this is called 'negative real returns'. This means that by not investing or substantially increasing your income, you run the risk of not being able to continue living the same way. You will then have to adjust your lifestyle by, for example, spending less or saving on holidays, energy costs, etc. Simply because your money is worth less and at the same time the return on your money is too low to compensate for that.

People therefore divide their assets into different terms and goals. But instead of using different piggy banks, they use the distribution to make parts of their assets yield returns. That is smart asset allocation. A few tips:

☂️ The starting point is to have a financial buffer. Your buffer should cover about 6 months of your living expenses. You decide how critical this is and put this money in an account that you can easily access.

🧦 You should only invest in stocks with money that you do not expect to spend in the next five years. Make sure you set goals for your plan that need five years or longer, such as education, a sabbatical or perhaps retirement or a world trip.

🏠 Buying a house in the future is a possible exception to your five-year rule for investing. This is because there is increasing similarity between the stock and housing market. So it may pay to start a plan for a house now and use this money for the purchase in the future, even if it is within the five-year rule.

So what do I have to do?

Are you considering starting to invest, do you have money besides your buffer that you can spare, or have you sold some of your crypto? Then you could use that capital to gradually (periodically) build up a diversified portfolio over the next 6-12 months. Consider the following when making a plan:

- Ensure a long investment horizon.

This way you don't have to worry about a bad week, month or even year.

- Evaluate your goals every six months.

Are you still on track to achieve your goals or determine what you want to do with new savings?

- Manage your risk so it doesn't manage you.

Create peace and focus by determining in advance how much risk you can take to achieve your goal.

- Create a diversified portfolio.

Determine the type of investments to invest in a diversified (and, for example, sustainable) manner.

Vive helps you invest for the future

No knowledge, time or desire to create a plan yourself, but ready to invest? With Vive you can create a free investment plan. For every goal you have, you can create a plan in minutes, so you can achieve that goal in the best way possible. Compare it to a car navigation system that knows the best way to get to your destination. That plan is fully customized to your financial situation, the market and your goals. In our opinion, the best way to build wealth for the future. You then decide whether we execute and maintain it for you.

Your plan advisor

With Vive you get access to unique asset management features such as the plan advisor who gives tips to improve your plans. Our plan advisor gives real-time insight into how your plans are doing and whether you need to adjust to achieve your goal. Or if the markets are not performing as expected.

Because your plans are monitored, you don't have to do the rebalancing yourself. As an asset manager, Vive monitors your plans day and night and ensures that the necessary actions are taken to keep you on course. Aye aye captain!

What does the World Cup have to do with this?

If we have learned anything from the football matches at the World Cup in Qatar, it is that the outcome can totally deviate from expectations. Predicting events or the outcome is impossible. Ultimately, the best strategy is to make a plan and ensure good diversification of your investments. This way you will eventually win all the matches.

🌱

Good to know

Vive's expressions are composed to inform and entertain. The content should not be considered financial advice. Do not take unnecessary risks and always read the essential investor information beforehand. Investing involves risks.

maak een afspraak

Klaar voor een moderne oplossing voor pensioen of vermogen? Maak vrijblijvend kennis met Vive en ontdek wat kan - voor jouw organisatie.

Complex pensioen, simpel uitgelegd - weet direct waar je staat

Persoonlijk gesprek voor jouw situatie en die van je werkenemers

In 30 minuten meer duidelijkheid dan uren googlen

Alle ruimte voor vragen aan onze ervaren pensioenexperts